Collab Fund

As a prominent capital source for forward-thinking entrepreneurs, Collab Fund encourages innovation that paves the way for a better world.

If I told you a company was on track for $500M in sales in 2024 — up from $200M in 2023 and $70M in 2022 — and thriving thanks to massive secular tailwinds, what kind of business would you imagine? A cutting-edge AI company? What if I told you it was a soda company founded just five years ago in Oakland, California?

The flashiest companies don’t always deliver the highest returns for early investors. Let’s explore a comparison between two vastly different businesses: OpenAI and OLIPOP.

OpenAI is among the most influential and widely discussed companies in the world, and for good reason. It ushered in a golden age of LLMs, with staggering ripple effects: skyrocketing AI-related CapEx among tech giants, NVIDIA’s ascent to the world’s most valuable company by market cap (though it now ranks #3), and a dramatic resurgence in U.S. power demand growth.

Then there’s OLIPOP – a soda company. But not just any soda. OLIPOP makes a healthier alternative with gut-friendly prebiotics and plant fiber. Its nostalgic flavors, like Classic Root Beer and Vintage Cola, feel indulgent but deliver a BFY experience. It’s also delicious. Simple as that.

Comparison methodology

To compare the investment performance of OpenAI and OLIPOP’s first investors, we’ll use a simple returns multiple: the current value of their ownership divided by their initial investment. Since both companies raised their first rounds in 2019, this approach allows for a direct comparison, even though it doesn’t factor in timing (e.g., IRR).

For simplicity, we assume early investors did not participate in later rounds and were diluted. To calculate these returns, we need to determine:

- Size and valuation of each company’s initial equity round

- Sizes and valuations of subsequent rounds to account for dilution

- A reasonable estimate of their current valuations

- A projection of future dilution each company may face before exit

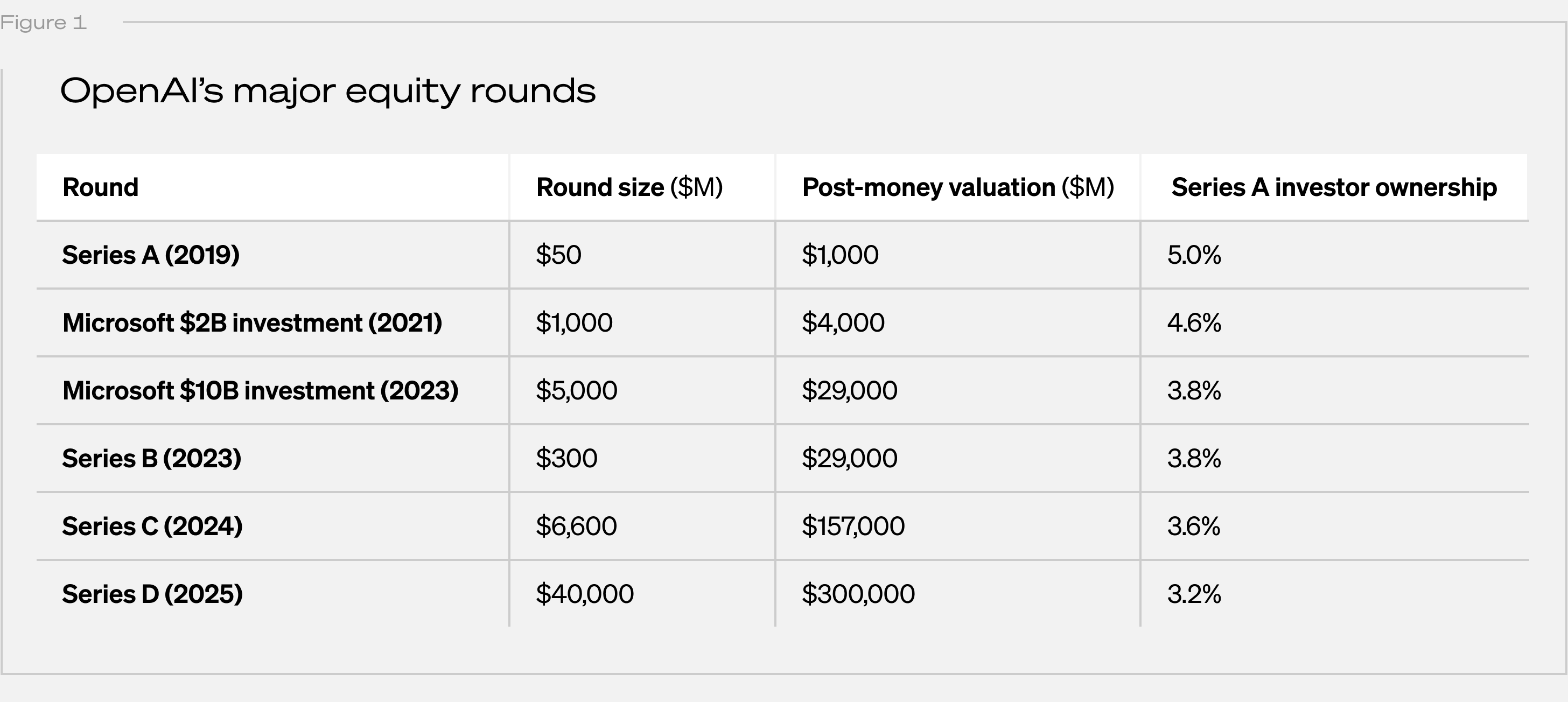

OpenAI’s returns

Founded in 2015 as a nonprofit focused on advancing AI safely, OpenAI restructured in 2019 to fund its expensive pursuit of AGI. It created OpenAI LP, a “capped-profit” entity governed by the original nonprofit (renamed OpenAI Nonprofit). This structure allowed OpenAI to raise private capital while capping early investor returns at 100x, with any excess profits flowing back to the nonprofit.

At the time of this change, OpenAI also announced its first institutional funding round, led by Khosla Ventures. Let’s call this their Series A. Details remain unclear: PitchBook lists it as a $10M raise at an undisclosed valuation, while other sources suggest Khosla’s stake alone was $50M at a post-money valuation of $1B. We’ll assume a round size of $50M for 5% ownership.

Estimating dilution is tricky. Most of OpenAI’s funding post-Series A has been from Microsoft, which has poured in ~$14B through a mix of equity, Azure credits, and unique profit-sharing agreements. Sources disagree on the details, but key reported investments include $2B in 2021 and $10B in 2023. Adding to the complexity, OpenAI is now transitioning to a for-profit public benefit corporation, which could eliminate the 100x cap on early investor returns.

To simplify, we’ll assume:

- OpenAI completes its transition, removing the 100x cap.

- Half of Microsoft’s 2021 and 2023 investments were dilutive, with valuations of $14B in 2021 and $29B in 2023 (as suggested here).

Beyond Microsoft, OpenAI raised a $300M round in 2023 at ~$29B (Series B) and a $6.6B round in 2024 at $157B (Series C). Just yesterday, WSJ reported that OpenAI is in talks for a $40B round at a whopping $300B valuation (Series D). If this round closes as reported, Series A investors will be diluted from 5% to 3.2%, as shown in the table below.

At a $300B valuation, that 3.2% stake is now worth $9.5B – a 189x return on their initial $50M. Not bad!

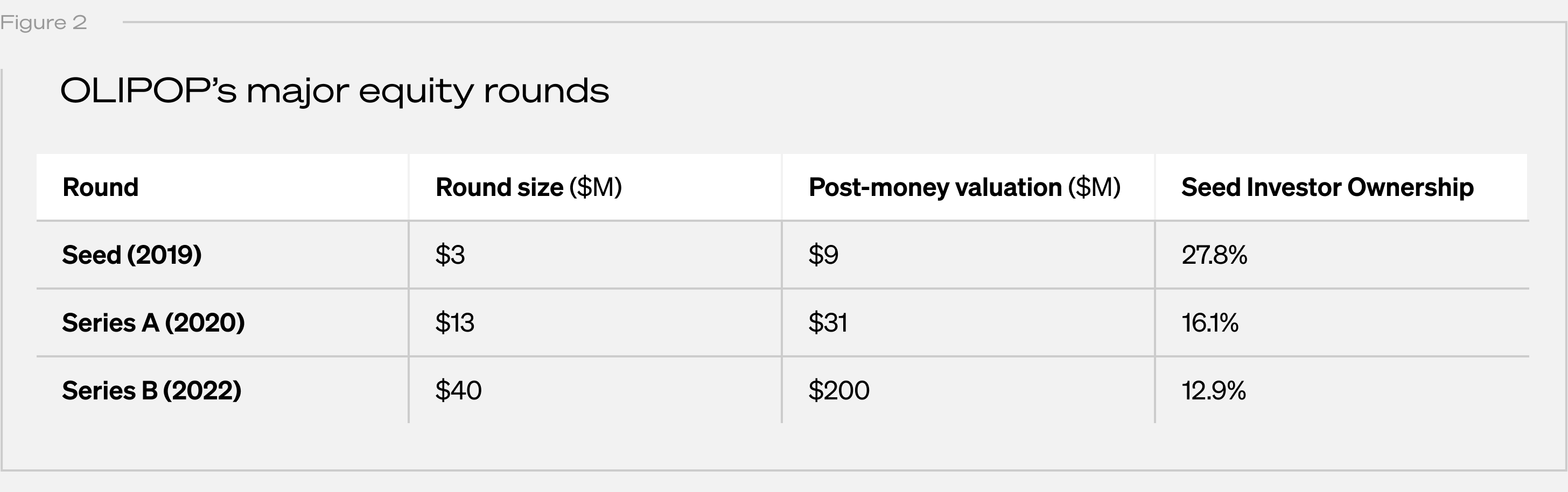

OLIPOP’s returns

OLIPOP’s story is far more straightforward. PitchBook shows its major funding rounds below:

OLIPOP’s seed investors have been diluted from an initial 28% ownership to roughly 13% today. The last disclosed valuation was during its 2022 Series B, but OLIPOP has grown significantly since then. To estimate its current valuation, we apply a forward revenue multiple from a public comparable to its projected next-twelve-months (NTM) revenue.

OLIPOP’s revenue growth has been remarkable, with several sources indicating it was on track for $500M in 2024 sales, up from $200M in 2023, and $73.4M in 2022. Extrapolating this 2022-2024 CAGR, we estimate NTM revenue of $1.3B. This projection seems reasonable, as revenue growth has shown little sign of slowing, and OLIPOP has significant room to expand distribution and retail presence.

Celsius Holdings (CELH), the maker of CELSIUS energy drinks, offers one of the only relevant public comparables. Applying their 3.8x forward revenue multiple to OLIPOP’s estimated NTM revenue yields an implied valuation of $5.0B.

At this valuation, seed investors’ 13% stake would be worth $639M – an astonishing 256x return on their $2.5M investment, outperforming even the 189x return estimated for OpenAI’s Series A investors.

Future dilution

While current valuations provide a snapshot, returns are realized at the point of liquidity. OLIPOP not only appears likely to deliver higher returns than OpenAI based on current valuations, but is also likely to experience less dilution – and the resulting erosion of returns multiples – before exit. To assess dilution risk, we must evaluate how much additional capital each will need to reach self-sufficiency, where revenues consistently cover operating and capital expenses. Ultimately, this hinges on the strength of each company’s unit economics.

OpenAI’s unit economics

OpenAI’s two primary revenue streams — ChatGPT subscriptions and API usage — present distinct unit economic profiles and associated challenges.

ChatGPT Subscriptions

OpenAI offers several subscription tiers, from a free plan with limited features to a $200/month “Pro” plan. While paid tiers generate predictable monthly revenue, inference compute costs scale with user activity, which can be unpredictable. This means new users don’t always equate to profit growth. This challenge is exemplified by recent reports that OpenAI is losing money on GPT Pro users due to unexpectedly high inference costs, despite the $200/month price point, which Altman set with profitability in mind.

This issue is further exacerbated by the overwhelming proportion of free-tier users – estimated at 95% – who incur inference costs without generating revenue. As a result, paying users effectively subsidize these expenses. Inference compute costs for 2024 were projected at $2B, compared to an estimated $4B in total revenue.

API Usage

The API’s pay-per-token model better aligns revenue with costs, but rising competition has eroded OpenAI’s pricing power. Token prices have plunged 89% in just 17 months, dropping from $36 per million tokens at GPT-4’s launch in March 2023 to $4 by August 2024. DeepSeek, which recently demonstrated that training and inference can be far less compute-intensive, has only accelerated this price collapse. Its reasoning and chat models are currently priced over 95% lower than OpenAI’s.

Training, while not directly tied to unit economics since it doesn’t scale with usage, remains a significant and growing financial burden. Costs are projected to reach $9.5B annually by 2026, with R&D expenses climbing from $1B in 2024 to over $5B in 2026. Though these projections predate DeepSeek’s breakthroughs in cost-efficient training, training will undoubtedly remain a massive and essential expense for sustaining AI leadership.

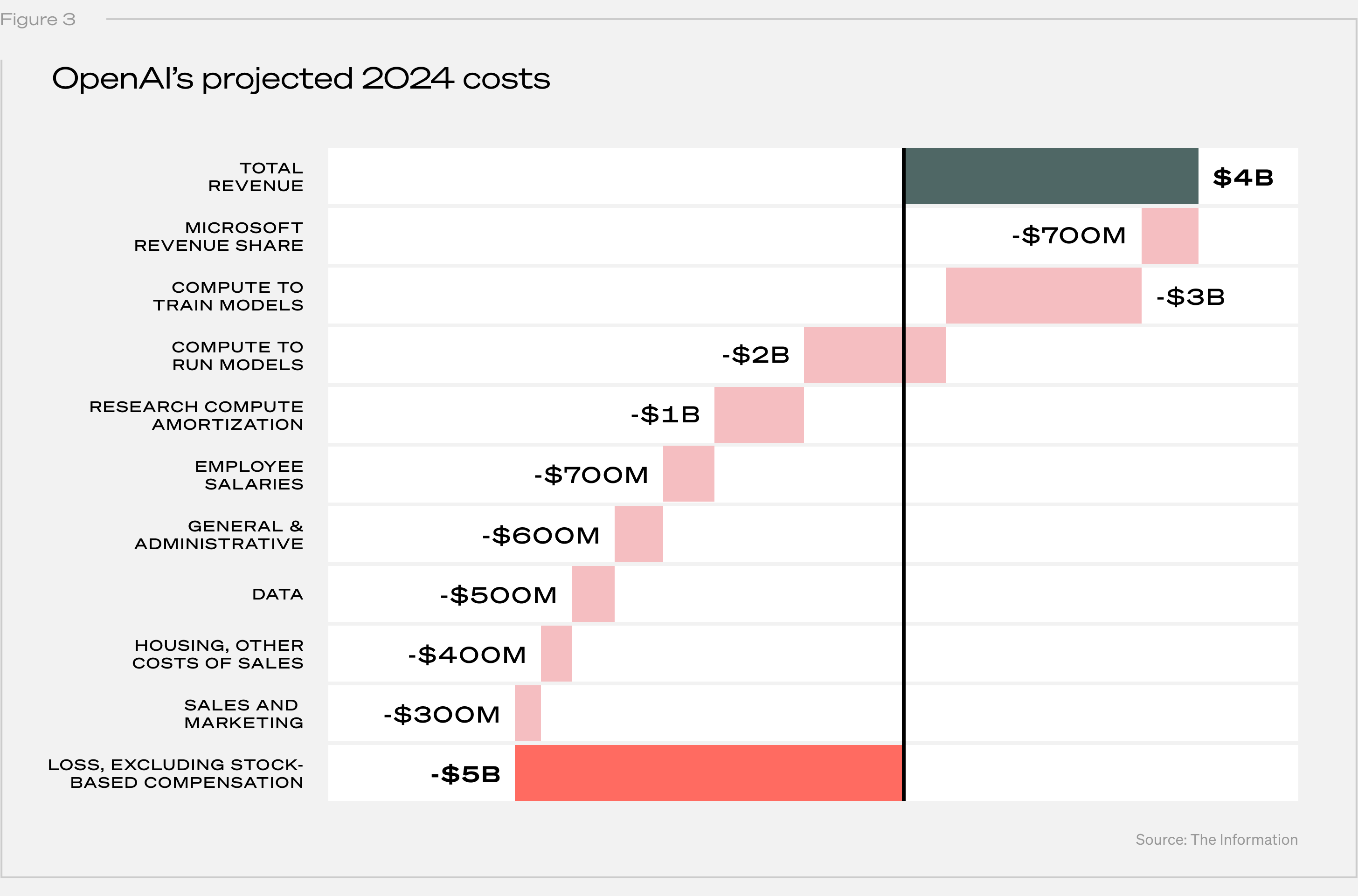

The following chart illustrates how high inference and training costs, a large base of free-tier users, and pricing pressures combine to create significant profitability challenges.

Training compute costs for 2024 were projected at $3B, with inference costs adding another $2B. Combined with Microsoft’s $700M revenue share and substantial operational expenses, these factors contribute to an estimated $5B loss for 2024, excluding stock-based compensation. These losses are expected to continue, with OpenAI projecting $44B in cumulative losses from 2023 to 2028. Profitability is targeted by 2029, with a revenue goal of $100B.

Covering these massive losses has required successive capital raises, most recently the $40B round, further diluting investors. If OpenAI’s $44B in projected losses through 2028 proves accurate, this latest capital infusion would have brought it close to self-sufficiency. However, a substantial portion of this round is reportedly allocated to OpenAI’s $19B commitment to President Trump’s $500B Stargate initiative, leaving a funding gap. As a result, more funding rounds and investor dilution are likely.

OLIPOP’s unit economics

OLIPOP benefits from straightforward unit economics, driven by predictable production and distribution costs in the established soda industry. Key variable costs include raw ingredients, packaging, co-packing fees, and freight, while fixed costs cover overhead, staff, brand marketing, and R&D. Unlike OpenAI, OLIPOP doesn’t require massive upfront capital or speculative R&D. Its differentiated formulation, brand identity, and consumer positioning also help shield it from commoditization risks despite competition from peers like POPPI.

Regarding future dilution, OLIPOP is already fully profitable. While the company is likely to raise additional capital to accelerate growth, they don’t need to. This gives a more flexible path to exit – OLIPOP could sell to a strategic buyer or IPO without the pressure of hitting complex, multi-year milestones. Fewer funding rounds, less dilution, and a profitable business model mean early OLIPOP investors are far less exposed to the risk of a delayed exit and ownership erosion over time.

Final thoughts

These returns underscore an important lesson: less flashy businesses can sometimes outperform even the most hyped tech companies. This is largely driven by the importance of entry price – achieving a 256x return is far more feasible from a $2.5M starting valuation than from $1B – as well as the path to profitability and the unit economics that pave the way.

While OpenAI is revolutionizing industries, OLIPOP is quietly dominating its category, proving that exceptional returns don’t always come from the highest-profile companies. For investors, the takeaway is clear – entry price and timing are critical, but so is recognizing opportunity in unexpected places.

Finally, full disclosure – Collaborative Fund is a Seed investor in OLIPOP – an investment made before I joined the team. Credit goes to my colleagues for identifying the opportunity early, and even more to the OLIPOP team for consistently exceeding expectations.

If this has left you craving OLIPOP or curious to learn more, you can check them out here. My favorite flavor is Vintage Cola.

“Our political leaders will know our priorities only if we tell them, again and again, and if those priorities begin to show up in the polls.”

— Peggy Noonan

Ahead of Thanksgiving, I thought it would be timely to write about something every American should be thankful for, so here it goes.

The United States just concluded its 60th presidential election and every American should be thankful.

Now, before everyone who voted for Kamala Harris starts to fume, hear me out.

The reality is that every American should be thankful after every election, regardless of the outcome.

You heard that right.

Every American should be thankful after every election. In fact, every American should also be thankful that these elections are often determined by razor thin margins.

Why?

Because these elections highlight one of America’s greatest superpowers – its “optionality”.

Let me explain.

Optionality is defined as, “The ability, but not the obligation, to choose a specific path.”

America’s optionality stems from the fact that its citizens have the ability, but not the obligation, to change the country’s direction every four years. If things are going well, Americans can choose to “stay the course”. However, if they believe the party occupying the White House has swung too far in one direction, they can vote to move the country in a different one.

Don’t get me wrong. America has a lot else going for it, including being protected by two massive oceans on its coasts and two friendly nations to its north and south, vast resources (energy, farmland, and navigable waterways), a diverse population, an educated workforce and entrepreneurial ethos, and the world’s strongest military, economy, and financial markets. However, Americans’ ability to choose how to leverage these assets most effectively is what makes it the most dynamic country and economy in the world.

As to why Americans should be thankful that their elections are determined by razor thin margins, the fact is that if America had one dominant political party (i.e. “one party rule”), it would be much more difficult to enact change. Thankfully though, American swing voters play an instrumental part in how the country is run, as evidenced by the most recent election.

Now, a logical response would be,

“But don’t these razor-thin margins lead to elevated tension, friction, and division, especially in the lead up to and after elections?”

Of course, but that is because optionality isn’t free. In fact, it always comes with a cost. Yet, the tension and division associated with optionality is almost always cheaper than the alternative.

Look no further than Argentina.

A century ago, Argentina was one of the strongest and wealthiest countries in the world. With endless resources, a diverse and literate population, and a diversified industrial base, Argentina was positioned for an incredibly bright future. European nations had started investing heavily, while countless multinational companies were opening offices or plants throughout the country (including manufacturing, retail, advertising, construction, and finance companies, as well as law firms). Some even declared its capital, Buenos Aires, “The Next Paris”.

Then, everything began to change.

In 1913 Argentina suffered a coup d’état, which was followed by a series of government overthrows that resulted in alternating periods of democracy and military rule. Then, with the rise of Peronism in the mid-1940’s, the country embarked in what amounted to more than 75 years of “one-party rule”.

The result?

Argentina went from being one of the world’s wealthiest countries in the world as measured on a GDP-per-capita basis to one ravaged by inflation (regularly north of 20% and over 100% in 2023), corruption, poverty (currently over 40%), and a rolling series of debt defaults.

So, how did this happen?

It happened because Argentinians lost their optionality. They lost their ability to institute change. To shape their destiny. As a result, a country many thought would be one of the next great global powers instead suffered a historic decline.

Sound familiar to something we are witnessing today?

It should, because after Xi Jinping removed term limits and instilled himself as “president for life” in 2018, the Chinese people were stripped of their optionality (while the Chinese do not have democratic elections, its leaders in the years prior to Xi typically responded to the needs/wants of the Chinese people and were chosen by consensus every ten years).

In doing so, Xi appears to have put China on a path similar to Argentina, or for that matter Russia, Turkey, Iran, and many Middle Eastern countries that are currently one-party or autocratic states. Unsurprisingly, these are the countries saddled with corruption, unbalanced economies, and on poor terms with the “West”.

Meanwhile nations with the most vibrant democracies, and therefore optionality (e.g., countries like Australia, Denmark, Finland, The Netherlands, New Zealand, Norway, Sweden, Switzerland, and the UK) are also the least corrupt, have the most balanced and resilient economies, and are some of the United States’ strongest allies. Unsurprisingly, these nations have also historically had some of the strongest equity markets.

Funny how that works.

The fact is, optionality is one of the most underappreciated things in life. It is what enables you to be nimble, change course, adjust on the fly, and self-correct. It is also what allows you to get through difficult moments, while simultaneously participating in the good ones.

While Americans may fight over the country’s path forward, be vicious with one another at times, and either get upset when their candidate loses or thrilled when they win, we should cherish our elections because it means we have the ability (but not the obligation) to change the path we are on. To choose our destiny.

As it relates to China, so long as optionality is absent, consumer confidence will remain depressed (has fallen more than 30% since Xi removed term limits), net capital outflows will continue, economic conditions will likely deteriorate further, and its equity markets will languish.

Frankly, this is what makes the country feel un-investable to me right now.

That said, if China reverts to a system of term limits, things could change quickly and dramatically.

After all, this is precisely what has happened in Argentina after its citizens elected libertarian Javier Milei last year. The results so far have been astounding as Argentina has experienced a material drop in inflation, green shoots in economic growth, and world leading equity returns as a result of his sweeping changes.

Often times the things we should be most thankful for aren’t obvious because they come with a cost. In the case of our elections, the cost is more than well worth it.

Ryan McFarland came from a long line of motorsports junkies given that his grandfather had been a race car engineer and his father ran a motorbike store. As a result, it shouldn’t come as a surprise that McFarland grew up riding dirt bikes and stockcars, or that he eventually went into the family business as well. It also shouldn’t come as a surprise that he was eager to pass on the McFarland “love of wheels” to his own son.

As any parent knows, getting a young child to ride a bike is a significant challenge. McFarland’s experience was no different. So, like many of us, he purchased an endless number of things to help his son get riding — toddler tricycles, trainer bikes, and even a training wheel equipped motorcycle.

Nothing worked. More importantly, each failed to teach his son the most important part of riding a bike — learning how to balance.

Think about it. While training wheels or a tricycle might stabilize a rider, neither allow a kid to equalize their weight on a bike.

The reason?

The extra wheels do all the balancing. They simply serve as a crutch.

So what did McFarland do?

He decided to engineer a very different type of bike, but rather than adding something to the bike, he chose to take something away — in this case the pedals.

The result was the Strider Bike, which enabled kids to focus exclusively on their balance and has since become one of the best-selling bikes of all-time, as well as a godsend for parents everywhere.

Within a few days, McFarland’s son was riding the Strider Bike. Within a couple weeks, he was riding a real bike. Within a few years, his company had sold millions of bikes. In short, McFarland had solved a significant challenge with a simple (and far less expensive) solution.

This story is far from the only case where the best solution came from using less of something rather than more. In fact, I have dealt with this dynamic personally over the past two years.

See, I grew up with eczema as a child, which I thankfully outgrew when I was about eight years old. Unfortunately, it reappeared in patches back in early 2021, so I went to see numerous doctors, dermatologists, and allergists. Each recommended a new cream, pill, and eventually a shot, which led to very mixed results. Finally it dawned on me to ask an allergist for a patch test, which is essentially a way to test to see if you are allergic to any specific chemicals that are commonly found in various soaps, shampoos, creams, and countless other products. I took the test and found out I was very allergic to two of the 150 things they tested for, one of which is prevalent in something called Aquaphor, which is a Vaseline-like ointment that we had been using on my both of my sons’ skin.

Care to guess when we had started using it?

You guessed it, early 2021. Precisely the same time that I started having a recurrence of my eczema.

So, what did we do?

We removed Aquaphor from daily use in our house, I stopped taking the various medications I was using, and my skin problems have slowly improved.

Whether it applies to training wheels or skin medication, this begs the question — why are we so inclined to add things rather than take them away when searching for solutions?

The answer is simple — human nature and incentives.

The fact is, people are biased towards solving problems through addition rather than subtraction.

The reason?

Because adding something makes you feel like you are advancing, while taking something away makes you feel like you are retreating. Couple this with the fact that most companies are incentivized to sell us endless “solutions”, and it should come as no surprise that the desire take something away is practically non-existent.

We see this dynamic across all parts of the economy, and society at large.

In healthcare, nearly every condition people face is addressed by adding something. Have a skin issue? Try this cream. Having trouble sleeping? Take this pill. Can’t lose weight? Take this new injectable called Ozempic (ironically a drug that aims to *take away *our appetites). Casey Means wrote extensively about this in her new book — Good Energy — that is now #1 on the Amazon charts. In short, she makes the case that instead of jumping immediately to medications that almost always have side effects, we should instead start by identifying what is causing the problem and trying to eliminate it. For example, if you have a skin issue, start by cutting out soaps with countless active ingredients. Can’t sleep? Cut back the amount of alcohol you drink and/or TV you watch before bed. Dealing with a stomach or weight issue? Try reducing the amount of processed food and sugar you eat.

In software, this concept of favoring less over more is known as the “Mythical Man Month” (or more simply, “Brooks’ Law”), which was discussed at length on a recent podcast Patrick O’Shaughnessy did with Bret Taylor (Co-Founder of Sierra, former Co-CEO of Salesforce, and a current board member at Open AI). Taylor pointed out that,

“If you want to make a software project take longer, add more people to it. This is based on the premise that when you are developing a complex system, smaller teams who complete each others’ sentences, each own part of the system, truly understand it, and work in unison create a magical, yet fragile, dynamic. This is the case because adding more people means more bureaucracy, which risks disempowering some of your best people and slowing things down. Just look at Healthcare.gov as a perfect example.”

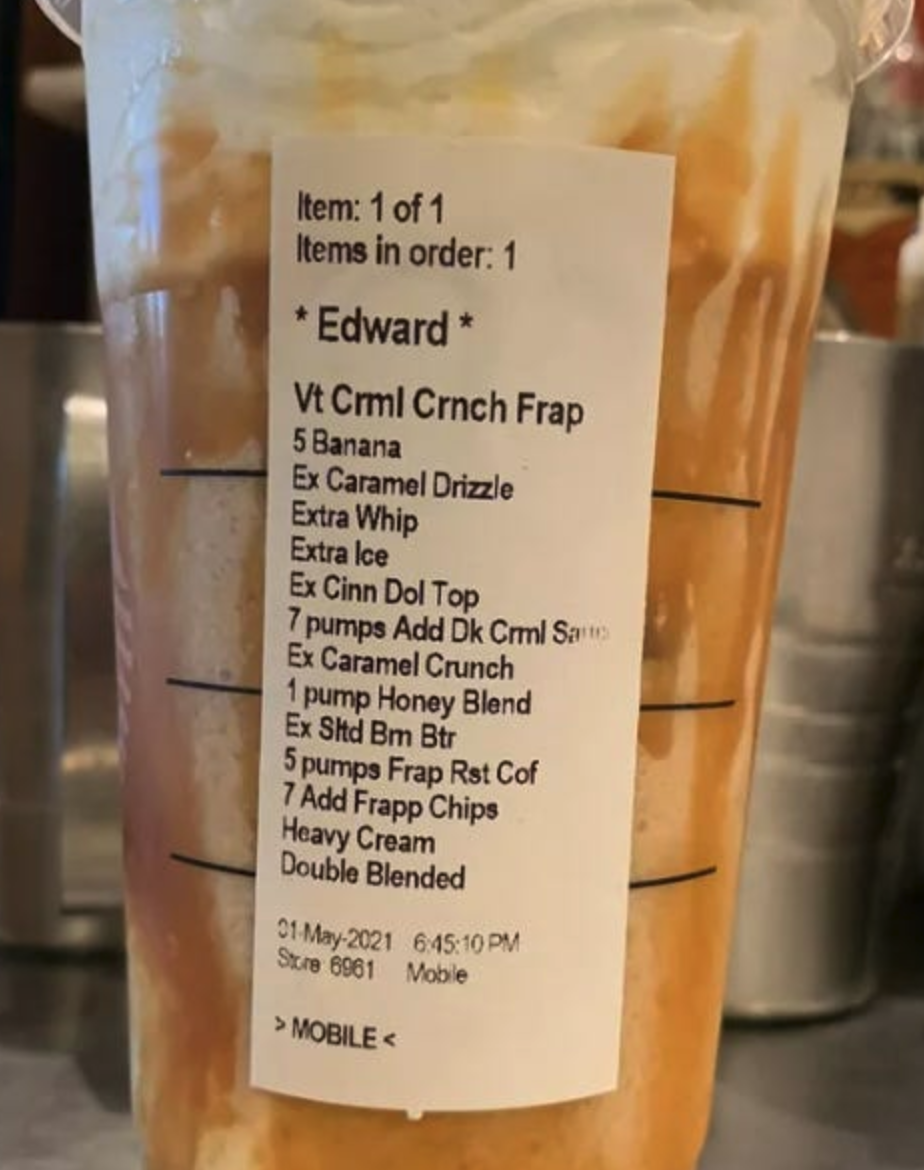

Retail is another obvious example. Look no further than Starbucks’ recent troubles. One of the main culprits? The decision to add countless options to their mobile app. In short, by designing its app to enable customers to hyper-customize their favorite drinks (according to one report there are over 170,000 ways to customize a Starbucks order), it led to orders like the one below:

Instead of increasing revenues and customer retention, this hyper customization led to poor customer service, employee turnover, longer wait times, and often incorrect drink orders. Eventually, it even led to Starbucks firing its CEO and replacing him with Brian Niccol, who made a name for himself running a company that has nearly perfected the concept of “taking things away” — Chipotle.

In short, by having far fewer options and ingredients, Chipotle created a juggernaut in the fast casual category by maximizing efficiency, throughput, and quality, which is a very different business model than a company like McDonalds, which has an endless number of options on its menu and is constantly adding new ones.

As a result, last year Chipotle’s restaurants collectively generated more than $10 billion in annual revenues and close to $2 billion in annual operating profits (up from $900 million and $250 million respectively fifteen years ago). This model has resulted in a stock that has compounded at more than 25% annually over the past decade-and-a-half, which means that $1,000 invested in 2009 would be worth more than $40,000 today.

Unfortunately, too many investors manage their portfolios like McDonalds or Starbucks instead of Chipotle. In an attempt to improve or upgrade them, they almost always look to layer on new investments, commitments, asset classes, and securities, often shooting well past an appropriate level of complexity:

Worried about a market crash? Layer on expensive hedges.

Concerned about volatility? Buy complicated options.

Want to generate higher returns in a low interest rate environment? Add leverage.

Trying to keep up with other investors? Chase a hot buyout or venture capital fund.

The trouble is that when they do this, the more vulnerable their portfolios become. It causes them to lose track of what they own, reduces their portfolio’s liquidity and transparency, and forces them to pay higher fees in the process. It also often leads to investors being forced to make decisions they swore they never would, typically at the worst possible moments.

We saw this first hand in the lead up to, and during, the Covid crazed market of 2020-2021. “One man band” venture capitalists were able to raise money with ease, firms like Tiger Global sprayed money in every direction with little diligence, term sheets from unknown investors landed on general partners’ desks, “extension funds” were waved into portfolios without even the slightest objection from limited partners, leverage was easy to come by, and investors happily traded daily liquidity for decade liquidity. Yet this is just the tip of the iceberg, as there were countless other examples of investments and structures being added to portfolios in pursuit of higher returns.

However, in 2022 and 2023, this dynamic changed materially as “one man VCs” started to disappear, the Tigers of the world were humbled and retrenched, those blind term sheets stopped coming, extension funds were tabled, limited partners starting guarding liquidity with their lives, and investors more broadly started pulling in the reins as they attempted to determine what lay ahead.

So, experiences like this beg a few questions:

Is increased complexity the path to better performance, or would investors be better off if they simply removed a few things?

Should investors hold one hundred 1% positions in their portfolio (i.e., be overly diversified), or should they concentrate their bets in their highest conviction positions, watch them closely, and add to them when they get dislocated?

Should investors deploy capital at a torrid pace during bull markets, or would they benefit from slowing down a bit?

The answer in each case is very likely an emphatic “yes” to the latter.

In fact, this probably goes for most things in life.

Think about it this way. What would happen if you reduced the number of things you focus on in your daily life by 20%? How about 30%?? Say 50%???

What are the chances you wouldn’t miss the things you cut out?

Would you possibly become more focused on the things you decided to keep?

Would you end up being a happier person? A better colleague? Parent? Spouse?

My guess is the answer would be a “yes” across the board here too.

But you might say, my life or portfolio is already SO complicated, how can I possibly uncomplicate it?

My response?

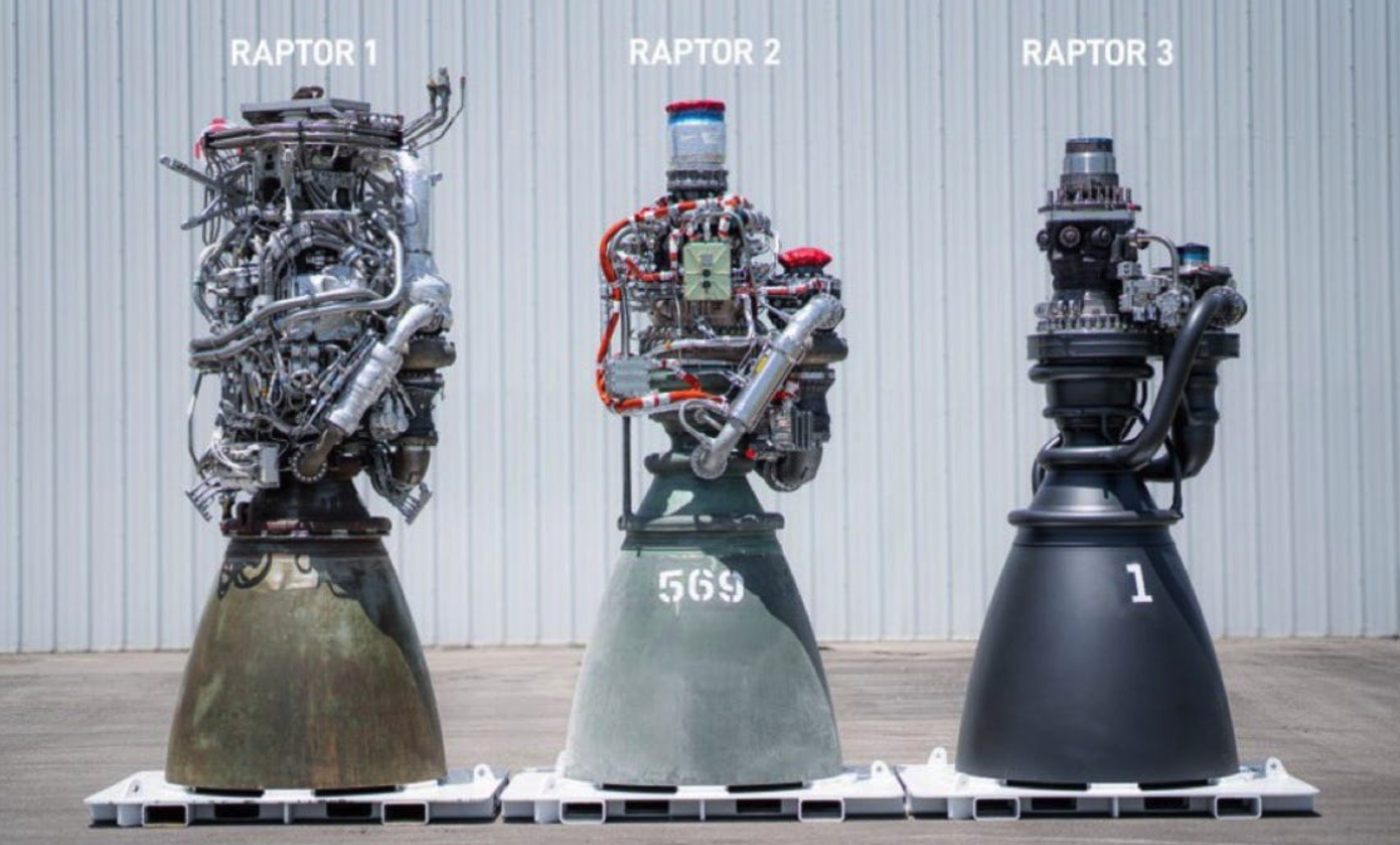

Just because things have gotten complicated doesn’t mean you can’t reverse it. Afterall, if Elon Musk can do it with his Raptor rocket engines, you can too.

In this day and age the case can be made that we live in an era of too much. Too much information, too much stuff, too many choices, and too many distractions. As a result, there is a good chance that the path to happier lives, and yes, better portfolio performance, might start by taking things away.