Collab Fund

As a prominent capital source for forward-thinking entrepreneurs, Collab Fund encourages innovation that paves the way for a better world.

Outrunning Giants: Building in OpenAI’s Shadow

From 2016-2021, a flurry of writing assistants, conversational chatbots, travel booking platforms, and meeting transcription tools popped up on the AI scene, many growing at breakneck paces.

And then along came ChatGPT’s steady rollout of new features: from freemium chatbots and writing tools in 2021 to, the release of Operator for booking in January 2025, and Record mode for meeting transcription in June 2025 — putting real strain on startups trying to compete.

This is a refrain I hear over and over in consumer AI investing: how can you build consumer applications when OpenAI has such a lion’s share of user attention (and data) to build any tool it wants.

When a single company begins to dominate a category, the instinct is to copy or cave. But the correct move is to find the spaces where the behemoth can’t compete. Where its own size might work against it. During Web 2.0, Google was that behemoth, bulldozing everything from Yahoo and MapQuest to AltaVista and AskJeeves. Still, e-commerce and social carved out their own ground beyond Google’s grasp.

Now OpenAI towers in consumer AI with hundreds of millions of weekly users and vast compute at its back. So where might value accrue outside its shadow?

The Gravity of the Giant

OpenAI’s ChatGPT has become a default destination for anyone exploring what consumer AI can do. Its freemium launch hit 1 million users in days and reached a record breaking 100 million MAUs in just two months.

What’s even more remarkable is the retention: over 80% of active users return regularly, and paid subscribers show retention north of 70% after six months.

That level of attention fuels personalization: the more you use it, the more it learns your patterns, preferences, and shortcuts. It’s human nature to stick with what feels familiar, but the ever-improving feedback loop of AI only magnifies that tendency. Consumer apps face both OpenAI’s head start and this natural stickiness. But just as Google could not put up a fight against Amazon and Facebook, there are areas where startups have the edge. Here are the three that I’m paying close attention to:

1. Vertical Trust and Domain Expertise

General-purpose chatbots struggle with high-stakes, regulated domains. Imagine asking for tax advice or mental health guidance from a generic model: liability concerns and nuanced regulations demand specialized expertise. In personal finance, healthcare, taxes, real estate and other fields built on trust, users need evidence of domain credibility. A startup that embeds clinicians, registered accountants, or licensed advisors into an AI workflow can differentiate.

The model may handle surface-level queries, but the human-vetted pipeline or validated data sources create a barrier OpenAI alone cannot clear without replicating specialized teams. It’s a classic dyanmic, but deep verticals reward focused players more than horizontal giants.

2. Bridging to the Physical World

As powerful as AI is, many high-value consumer experiences still benefit from (or even require) real-world integration. Startups like Doctronic show how AI triage leads to a telehealth session, then perhaps to in-person care. Travel can be reimagined: an AI plans an itinerary, but it also books local experiences, arranges guides, or curates surprise pop-ups — and then follows you there. Real estate might not just match listings and orchestrating visits, but guide you in real time through inspections, paperwork, and move-in services.

These require logistics, partnerships, and on-the-ground networks. The moat isn’t the model; it’s the operational backbone that connects AI suggestions to tangible outcomes. That’s a hard feat for a digital-first (and only) company like OpenAI.

3. Closing the Creativity Gap

A June 2025 study in Nature Human Behaviour investigated brainstorming tasks where participants used tools like ChatGPT versus relying on their own ideation plus web searches. It found that while AI can boost idea quantity, it often reduces variety: many AI-assisted participants produced very similar concepts, suggesting a “creativity gap” in generative models compared to unfettered human thinking. This echoes concerns that AI’s training on large but finite datasets drives convergence toward statistically common patterns, limiting novelty despite fluent output. Enhancing human creativity, mimicking human creativity will be tremendous efforts requiring specialized teams that think creatively themselves, and not just technically.

This isn’t to dismiss LLMs’ value (accelerating first drafts can meaningfully improve the creative process) but genuine creativity demands human curation, oddball connections, and serendipity. Startups that build tools to surface unexpected prompts, aggregate diverse human inputs, or structure hybrid workshops can capture value where vanilla AI falters.

Final Thoughts

It’s easy to feel outgunned by OpenAI’s budget and reach when single new feature release can eclipse months of effort. But success isn’t’ about trying to outscale OpenAI. It’s about finding places where AI is a means to something bigger. Giants excel at horizontal scale, but stumble on deep trust, real-world execution, or genuine novelty. That’s where value will continue to accrue. In the gaps that AI can’t fill.

Checklist for founders:

-

Trust gap: Which regulated domain do you know deeply? How will you embed vetted experts and compliance into your workflow?

-

Physical integration: What real-world services or partnerships can you build that a digital-first giant would find expensive to replicate?

-

Creative differentiation: How will you inject human serendipity or domain-specific inputs before or alongside AI to surface truly novel ideas?

-

Operational moat: What processes, partnerships, or data pipelines can you lock in early to defend against copycats?

-

User habit loops: How will you create feedback loops (e.g., personalized data, rewards) that cement engagement beyond a generic model’s appeal?

Lately, it feels like every corner of my internet bubble is talking about venture returns—Carta charts one day, leaked DPI tables the next. I’ve seen posts on lagging vintages, mega-fund bloat, the “Venture Arrogance Score”, the rising bar for 99th‑percentile exits, and the PE-ification of VC.

But for all that noise, I haven’t seen much that actually walks through how returns metrics evolve over time in an early-stage fund. That’s a crucial gap. Many analyses focus on funds that are still mid-vintage, where paper markups can tell an incomplete or even misleading story.

So I pulled the numbers on Collaborative’s first fund, a 2011 vintage that’s now nearly fully realized. It offers a concrete look at how venture performance can unfold across a fund’s full lifecycle.

Fund 1 was small: $8M deployed across 50 investments. Check sizes ranged from ~$10K to ~$400K, averaging around $100K for both initial and follow-on rounds. It was US-focused, sector-agnostic, and mostly pre-seed through Series A.

Portfolio metrics

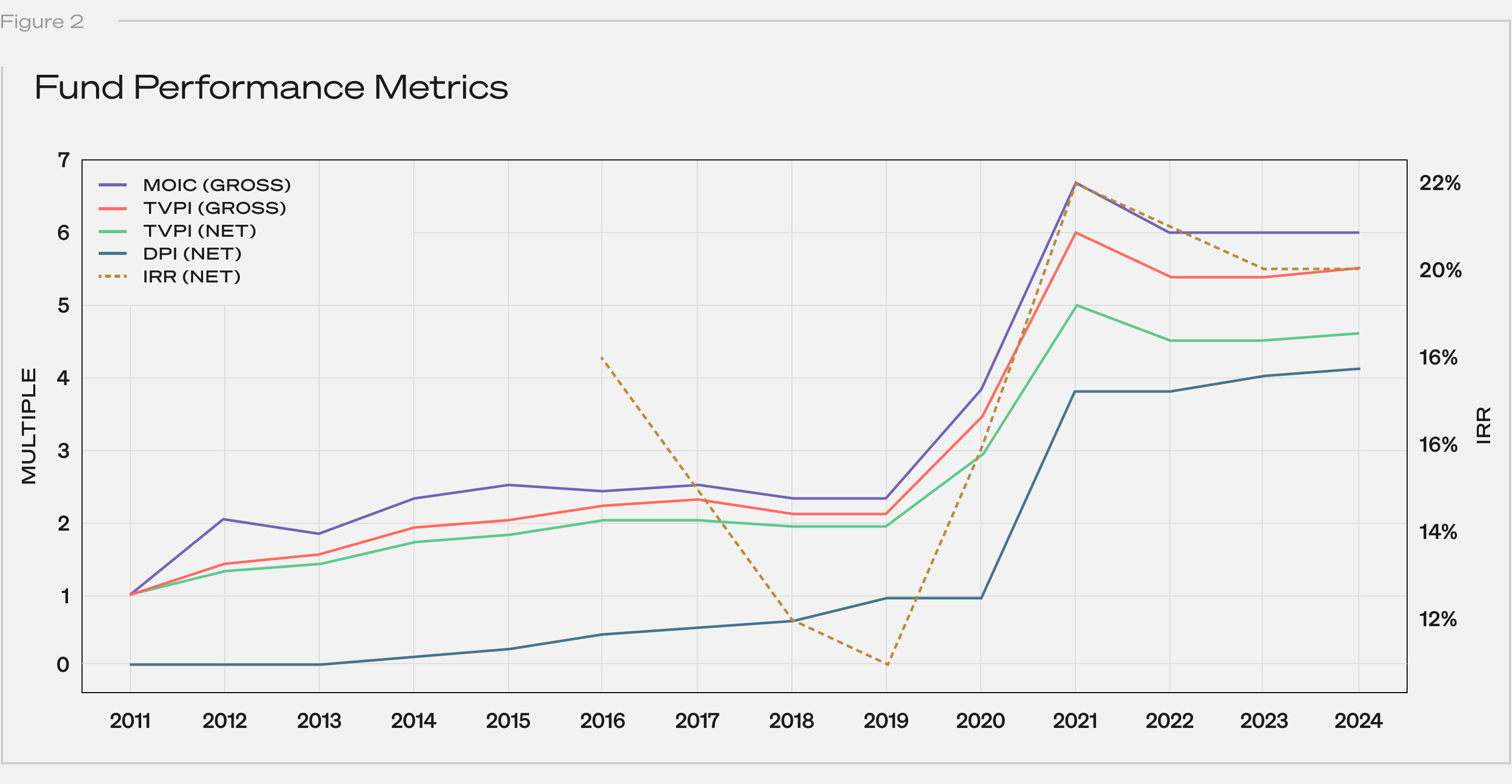

Without further ado, here’s how the fund performed over its lifetime across a few core metrics:

Note: Distributions are net to LPs; contributions reflect paid-in capital. IRR data was not meaningful (“NM”) for years 1–5.

Below is a line chart of the returns data:

Note: IRR is shown as a dashed line corresponding to the secondary axis.

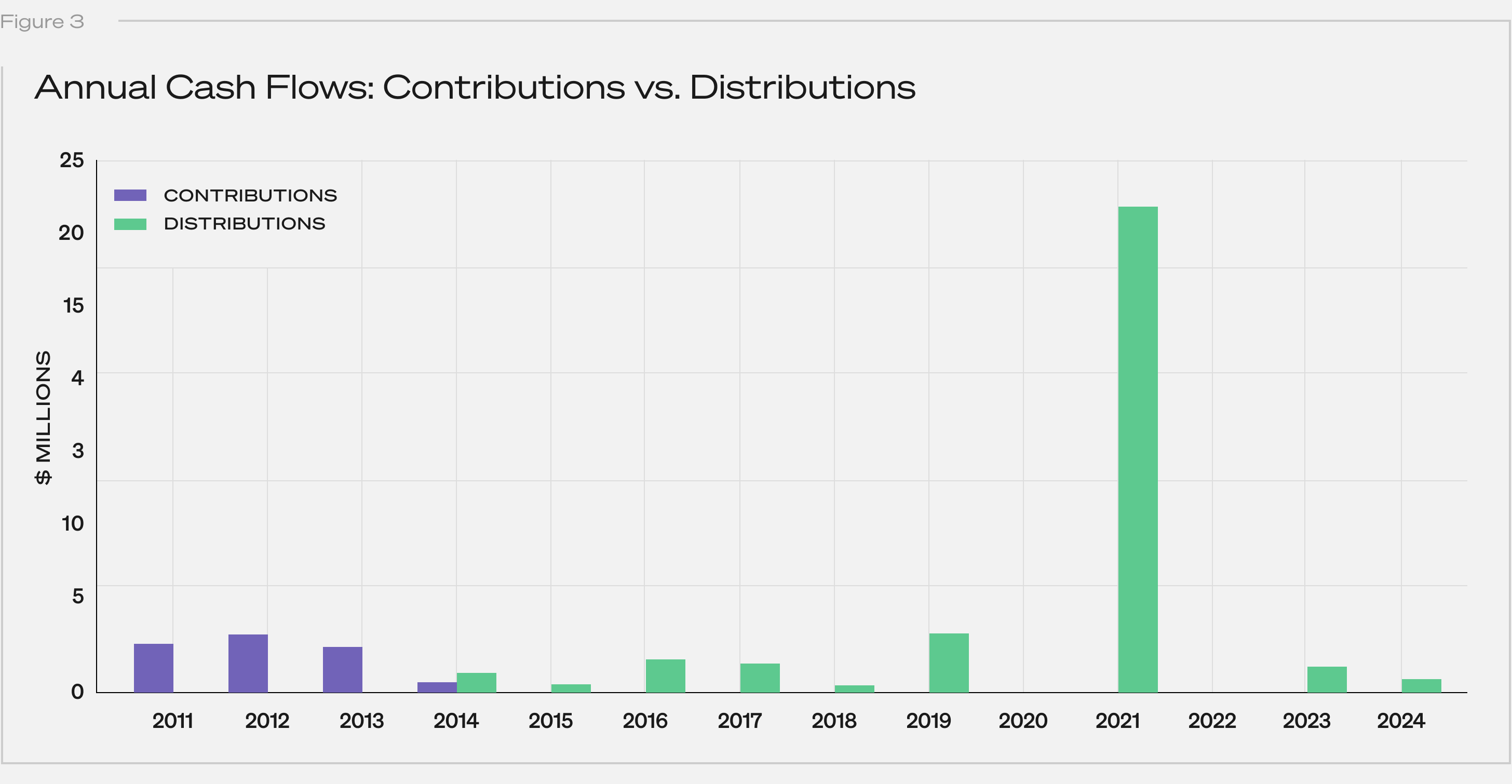

Contributions wrapped up by year 4, which is typical for early-stage funds. Distributions didn’t start until year 4 and peaked around year 10:

Returns metrics takeaways

- Strong overall performance: The fund achieved a 4.1x net DPI—solidly top-decile. For context, PitchBook pegs 3.0x as the 90th percentile for funds in the 2011 vintage.

- The patience premium: At year 10, DPI was 0.9x. There’s a lot of discussion right now around the lack of venture liquidity. 10 years in, this fund could’ve been a talking point. But then, in year 11, DPI jumped to 3.8x. Liquidity might be slow, but value can still be building.

- The IRR roller coaster: Net IRR hit 18% in year 6 (off paper gains), sagged in the middle years, then popped to 22% in year 11 after a major exit. IRR can be hurt by delays, even when final outcomes are strong.

- Some juice still left: Even after 14 years, the fund sits at 4.1x net DPI and 4.6x net TVPI. That means roughly 0.5x of upside is unrealized. That tees up the classic end‑of‑life question: seek to harvest the tail or ride it out?

- Shallow J-curve: Early markups lifted TVPI above 1x by Year 2, keeping LPs above water on paper even before distributions began.

Where did the DPI actually come from?

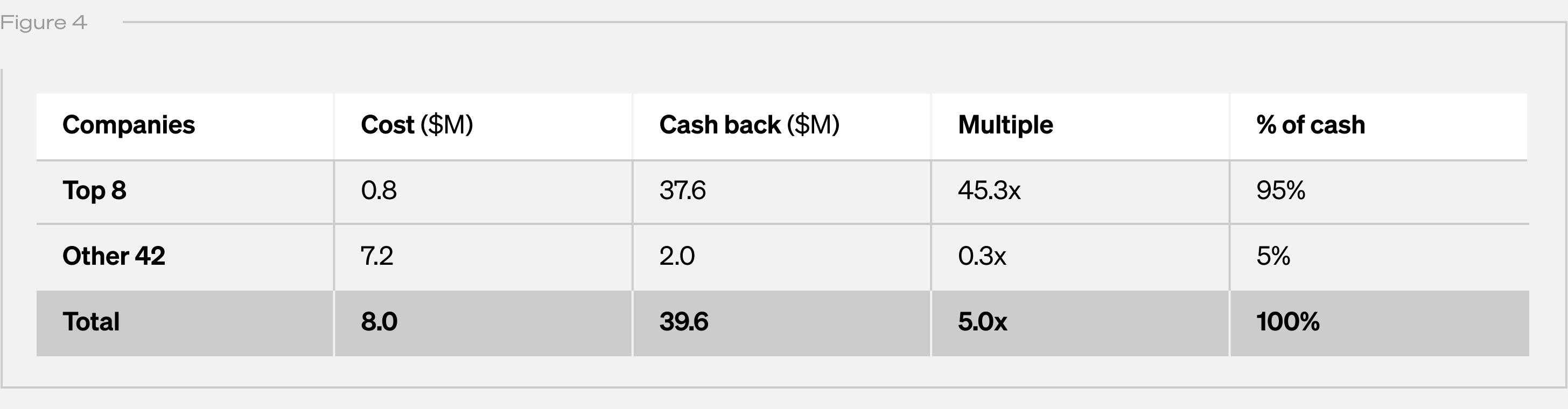

Returns were highly concentrated. Eight companies—Upstart, Lyft, Scopely, Blue Bottle Coffee, Maker Studios, Gumroad, Reddit, and Kickstarter—drove nearly all distributions.

Note: “Cost” is cumulative capital actually invested. “Cash Back” is cumulative proceeds received by the fund from realization events, and excludes (i) any remaining unrealized value and (ii) fund-level fees and expenses. “Multiple” is the quotient of Cash Back divided by Cost.

Together, these accounted for just $0.8M of invested capital but returned $37.6M—an average multiple of 45x. The remaining 42 investments, representing $7.2M, returned only $2.0M (a 0.3x multiple).

Within those eight, outcomes varied widely: one company alone delivered 73% of all cash returned. Adding the next three brought the cumulative share past 90%. Multiples ranged from 1.4x to 115x—illustrating just how concentrated and variable even a “winning” subset can be.

Portfolio lessons

- Power law: Eight companies drove ~95% of all returns. One contributed 73% on its own.

- Capital efficiency: Less than $1M into the top eight generated $37.6M back.

- Check size ≠ upside: Some of the biggest winners were sub-$100K checks, while some larger bets in the tail went to zero. Limiting ticket size can cap downside without necessarily hampering fund performance.

- Winner variance: Even among the winners, multiples ranged from low single digits up to well over 100x, underscoring that not every winner needs to be a moonshot but a few big outliers can matter tremendously.

Conclusion

We believe the biggest risk in early-stage VC isn’t failure. It’s missing (or mis-sizing) the outlier. In Fund I, eight companies drove nearly all distributions. One check alone accounted for more than 70% of DPI. This is the power law at work.

Collaborative’s story now spans 15 years with four early funds in harvest mode. Three rank in PitchBook’s top quartile with two in the top decile by DPI. In each, a small number of companies drove the bulk of returns. Perhaps these will make for future posts.

Until then, I hope this serves as a reminder to take venture performance narratives based on unrealized funds with a grain of salt. Some trends are real and worth watching. But many of the loudest signals may fade or reverse as funds mature. Until they’re fully played out, their stories are still being written.

Disclaimer: 1. This post is for illustrative purposes only. Certain statements contained herein reflect the subjective views and opinions of Collaborative Fund Management LLC (“Collab”). Such statements cannot be independently verified and are subject to change. In addition, there is no guarantee that all investments will exhibit characteristics that are consistent with the initiatives, standards, or metrics described herein. Certain portfolio companies shown herein are for illustrative purposes only and are a subset of Collab investments. Not all investments will have the same characteristics as the investments described herein. It should not be assumed that any investments identified and discussed herein were or will be profitable. 2. Certain information contained in this post constitutes “forward-looking statements” that can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “target,” “project,” “estimate,” “intend,” “continue,” or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of any Collab investment may differ materially from those reflected or contemplated in such forward-looking statements. 3. Performance as of December 31. 2024, unless otherwise noted. Past performance is not indicative of future results. There can be no assurance that any Collab investment or fund will achieve its objective or avoid substantial losses. Gross returns do not reflect the deduction of management fees, carried interest, expenses and other amounts borne by the investors, which will reduce returns and in the aggregate are expected to be substantial. References to “Net IRR” are to the internal rate of return calculated at the fund level. In addition, references to “Net IRR”, “Net TVPI” and “Net DPI” are calculated after payment of applicable management fees, carried interest and other applicable expenses. Internal rates of return are computed on a “dollar-weighted” basis, which takes into account the timing of cash flows, the amounts invested at any given time, and unrealized values as of the relevant valuation date. 4. The values of unrealized investments are estimated as of December 31. 2024, are inherently uncertain and subject to change. There is no guarantee that such value will be ultimately realized by an investment or that such value reflects the actual value of the investment. Actual realized proceeds on unrealized investments will depend on, among other factors, future operating costs, the value of the assets and market conditions at the time of disposition, any related transaction costs and the timing and manner of sale, all of which may differ from the assumptions on which the valuations reflected in the historical performance data contained herein are based. Accordingly, the actual realized proceeds on these unrealized investments may differ materially from the returns indicated herein and there can be no assurance that these values will ultimately be realized upon disposition of investments. Different methods of valuing investments and calculating returns may also provide materially different results. 5. For informational purposes only. Not a public solicitation. 6. References to performance rankings of the fund herein refer to PitchBook’s Venture Capital Benchmark rankings for all geographies and fund sizes with data as of Q4 2024.

Collaborative Fund recently launched AIR, a new kind of accelerator for design-led AI products. It draws inspiration from the institutions that reshaped creative possibility in their time, places that brought together unlikely collaborators at key moments of technological and cultural inflection.

As we recruit for the first cohort, we’re talking to people who had a hand in creating those lighting rod moments. A few weeks ago we asked Nicholas Negroponte, founder of the MIT Media Lab, to reflect on what happens when culture and technology collide to create new ways of thinking.

Today we’re talking to Tom McMurray, former General Partner at Sequoia, who helped shape Silicon Valley’s first golden age. Tom was an early investor in Yahoo, Redback Networks, C-Cube, NetApp—and, importantly, Nvidia. He now serves on multiple boards focused on science and impact. We spoke to him about pattern recognition, capital discipline, and why he’s an investor in AIR.

Craig Shapiro: Tom, you joined Sequoia just as the first Internet wave was forming. Your portfolio reads like a Hall of Fame roster. What were the core filters you used back then?

Tom McMurray: It was very clear where to invest in the networking space—bandwidth was in high demand. It was less clear in the pure Internet space. Our diligence process was pretty established so we continually developed more refined filters and leveraged off our core capability in chips and enterprise software. In the case of Nvidia we had what I call a Sequoia moment—that wonderful nonlinear diligence process where after parsing through the business, we reached a point where there’s only a single question left to decide. Our secret sauce was that we often knew many times more than the founders did about their business. We understood where the real risks were.

For companies like Nvidia, our expertise in semiconductors from investments in Cypress, Microchip, LSI Logic, and Cadence, plus our experience with gaming companies, meant the market risks were very low. We could easily do due diligence on the founders because many worked for friends of Sequoia Partners—this was our sweet spot in the 1990s. And in the Internet wave, we had special insight through our investments in Cisco and Yahoo. They were market pioneers who saw the world 3-5 years ahead of us. They pointed the way many times, and we just jumped on it.

Speaking of Nvidia, walk us through what happened when Jensen Huang first pitched Sequoia.

Wilf Corrigan, a Sequoia Technology Partner and CEO at LSI Logic (where Jensen worked before starting Nvidia), told him to talk to Don Valentine at Sequoia about his “chip idea.” Jensen pitched the evolving game world and the need for more performance. Honestly, I had no idea at that point why we should invest in the company. But we asked harder and harder questions about team, competition, distribution, and got solid answers.

About 90 minutes into the pitch, Pierre Lamond asked Jensen how big the chip was. Jensen said “12 mm.” Pierre looked at Don and Mark; they nodded, and we committed to the investment on the spot. We led the Series A and Mark joined the board. The rest is history.

The critical question wasn’t about market size or vision—it was “can they build the chip, get the performance, and the price point?” That’s why the chip size question was the deciding factor. The semiconductor partners at Sequoia—Don, Pierre, and Mark—understood the significance immediately.

Fast-forward to today. Collaborative Fund just launched AIR, an AI residency in New York. You are an investor! Why?

Because you’re reproducing the conditions that made Sequoia’s hallways electric in the ’90s—cross-pollination of builders, researchers, and designers who argue, prototype, and iterate in the same room. Great companies are rarely solo acts; they’re jazz ensembles riffing toward a common groove.

What early-stage pattern recognition from Sequoia days should our AIR founders tattoo on their whiteboards?

The secret is to lean on your wins, learn from them, apply it as you expand, iterate, and keep going.

“Stay cheap until it hurts.” Capital efficiency forces clarity. The companies that survived the dot-com crash had burn rates lower than their Series A checks.

Critics worry AI will erase jobs or amplify bias. You’ve seen every tech cycle: where’s your compass pointing?

Every wave starts messy. But history says two truths persist:

-

Jobs evolve faster than they evaporate. Cisco killed some circuit-switch jobs yet birthed the entire network-engineer class.

-

Bias follows data, not silicon. Fix the training data, and you fix 80 percent of the problem. That’s human homework, not machine destiny.

The “force for good” part kicks in when entrepreneurs bake guardrails into the business model, not just the codebase.

Last one. A founder walks into AIR with nothing but conviction. You’ve got one question before you decide to invest—what is it?

I’d look for that “Sequoia Moment”—where after all the questions about team, market, and technology, we identify the single critical factor that determines success. For Nvidia, it was “how many millimeters wide is the chip?” Sometimes, it’s these seemingly simple technical questions that reveal whether a company can execute on its vision.

Golden. Thanks, Tom. Here’s to building AI companies that deserve to exist.

And to founders who remember: progress isn’t inevitable—people make it so.